IMS, the mortgage loan… as you wish!

Over 90% pre-approval

Without any financial burden

Cost free credit evaluation

We disburse over 10% of mortgages nationwide

Over 90% pre-approval

Without any financial burden

Cost free credit evaluation

We disburse over 10% of mortgages nationwide

Why get a mortgage?

As a word, "loan" sometimes creates concern despite the fact that it is the most appropriate way to speed up an important purchase, such as that of a residence. However, with the right guidance from IMS, who will assess your real needs and capabilities, taking a home loan will prove to be the best solution for buying a property.

More specifically, the purposes for which one can take a home loan are the following:

- Purchase, construction, completion, extension, improvement, repair of residence

- Buying a plot of land

- Refinancing mortgages of other banks

Basic mortgage terminology

How can you get a mortgage loan?

In order to get a mortgage loan, you can either go directly to one or more banks or to a credit broker who maintains partnerships with banking institutions and will mediate to ensure a successful and profitable transaction.

What is a mortgage broker?

Or in other words: what is IMS. This is the intermediary who undertakes the entire particularly timeconsuming and careful procedure for issuing a loan. In this way, the potential borrower is relieved of most of the processes (saving effort and time), significantly increases the chances of his application being approved and ensures that the loan he receives will be sustainable.

Why turn to IMS?

IMS, as a mortgage broker, helps you make the right decisions to repay your loan without any concerns.

We dedicate the necessary time to:

- To fully understand your needs.

- To check your credit rating and present all your possible options.

- To train you and advise you safely, so that together we can formulate the best solution for your own special case.

- To ensure the most suitable loan for you.

The most important thing is that we are by your side throughout the process and offer you a personalized service.

The 7 steps for your home

In order to issue your mortgage loan, seven basic stages are followed, in which the qualified IMS consultants will guide you safely, consistently and with complete knowledge of the procedures...

Next step, after your meeting with one of the IMS advisors, is to send your application to the bank of your choice for the amount you wish to be financed. IMS proceeds to gather your financial data, we prepare our report and send the request to the bank for evaluation. It is noted that in order to proceed with the pre-approval request it does not require that you have ended up with a property.

After the bank evaluates your financial profile, your request receives a financial pre approval. The financial pre-approval is an official bank form, on which is written the amount pre-approved by the bank of your choice, with a specific time validity. It essentially confirms that it agrees to finance you for the amount you requested.

Having received the financial pre-approval and once you have settled on a property, the bank will proceed with its inspection. The bank’s lawyer checks the legal status of the property, the engineer checks that it is urban planning legal and will assess its current commercial value, based on which the final loan amount will be finalized.

After finalizing the financing amount, your request receives final approval, the bank form that essentially guarantees you the granting of a specific loan amount. You can now safely proceed to sign the purchase contract for the property.

The final approval is followed by the signing of the property purchase contract, its transfer to the mortgage registry / land office and its presentation to the bank. The bank checks the purchase contract and the borrower’s file again. The signing of the loan agreement essentially formalizes the terms and conditions of granting the housing loan.

After signing the loan agreement, there is an appointment with the bank’s lawyer in order to proceed with the registration of the pre-notation on the property purchase. Essentially, the pre-notation note is a form of mortgage and secures the bank, as it acts as a guarantee for the amount of the loan granted to the borrower.

The last step of the process is the disbursement of the amount to the customer’s account, who by issuing a two-line check pays the seller of the property and the mortgage loan process is completed by presenting the notarized payment deed to the bank.

The 7 steps for your home

In order to issue your mortgage loan, seven basic stages are followed, in which the qualified IMS consultants will guide you safely, consistently and with complete knowledge of the procedures...

Next step, after your meeting with one of the IMS advisors, is to send your application to the bank of your choice for the amount you wish to be financed. IMS proceeds to gather your financial data, we prepare our report and send the request to the bank for evaluation. It is noted that in order to proceed with the pre-approval request it does not require that you have ended up with a property.

After the bank evaluates your financial profile, your request receives a financial pre approval. The financial pre-approval is an official bank form, on which is written the amount pre-approved by the bank of your choice, with a specific time validity. It essentially confirms that it agrees to finance you for the amount you requested.

Having received the financial pre-approval and once you have settled on a property, the bank will proceed with its inspection. The bank’s lawyer checks the legal status of the property, the engineer checks that it is urban planning legal and will assess its current commercial value, based on which the final loan amount will be finalized.

After finalizing the financing amount, your request receives final approval, the bank form that essentially guarantees you the granting of a specific loan amount. You can now safely proceed to sign the purchase contract for the property.

The final approval is followed by the signing of the property purchase contract, its transfer to the mortgage registry / land office and its presentation to the bank. The bank checks the purchase contract and the borrower’s file again. The signing of the loan agreement essentially formalizes the terms and conditions of granting the housing loan.

After signing the loan agreement, there is an appointment with the bank’s lawyer in order to proceed with the registration of the pre-notation on the property purchase. Essentially, the pre-notation note is a form of mortgage and secures the bank, as it acts as a guarantee for the amount of the loan granted to the borrower.

The last step of the process is the disbursement of the amount to the customer’s account, who by issuing a two-line check pays the seller of the property and the mortgage loan process is completed by presenting the notarized payment deed to the bank.

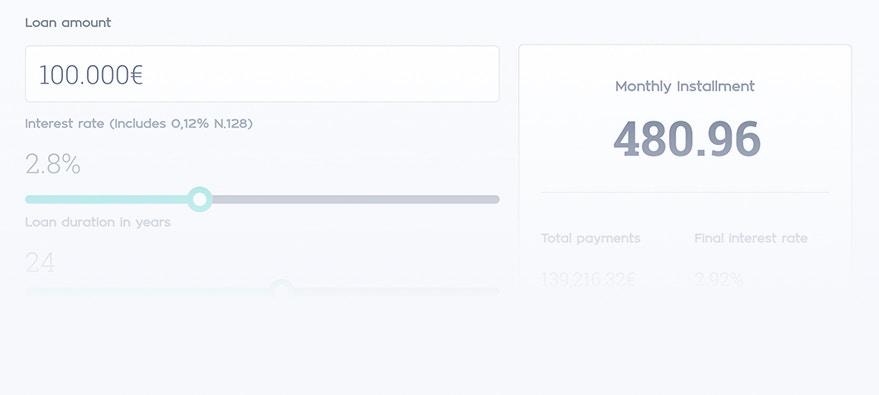

What mortgage are you interested in?